Employment data from May highlight regional gains

Lackluster wage and hours growth a sore spot in the stats

Update since Friday: no new indicators aside from the labor market statistics report that I’m writing about today. In the local papers, Jonathan Lansner wrote about these stats on Friday, noting the record-low 3.4% unemployment rate in San Bernardino and Riverside Counties, and solid job growth in goods transportation and warehousing. How low can the unemployment rate go? (Other parts of SoCal are as low as 2%.) Kevin Smith wrote about pay hikes for Wal-Mart pharmacy techs in California – yet more evidence of a strong labor market.

Even I was in the news this week! I had my monthly chat with Jonathan Linden at KVCR; segment and corresponding article (transcript) was published on Monday – see it here.

The BLS reports on jobs for 11 major industries for the region: mining and logging; construction; manufacturing; trade, transportation, and utilities; information; financial services; professional and business services; education and health services; leisure and hospitality; other services; and government. Aside from construction (down 0.7%), all sectors saw year-over-year job gains in May.

Overall, this was a very good report; thanks to the logistics industry, overall regional employment is back to pre-pandemic trend (some other areas haven’t even recovered all the jobs they lost during the pandemic!).

It’s not all highlights though: some industries in the region are still showing weakness, notably the public sector and goods-producing industries like manufacturing. This uneven recovery in jobs has caused the logistics industry to increase its share of employment in the region from 25.4% to 28% in just two years. I’ve written about the public school employment crisis before, and I’m sorry to say that this is still an issue (and perhaps should be read in tandem with drops in public K-12 school enrollment as well, which don’t show any signs of reversal; that link is strongly recommended by the way). We could see a jump this fall as schools finally start to revert to normalcy. As for manufacturing, I am not sure what can reverse the situation there.

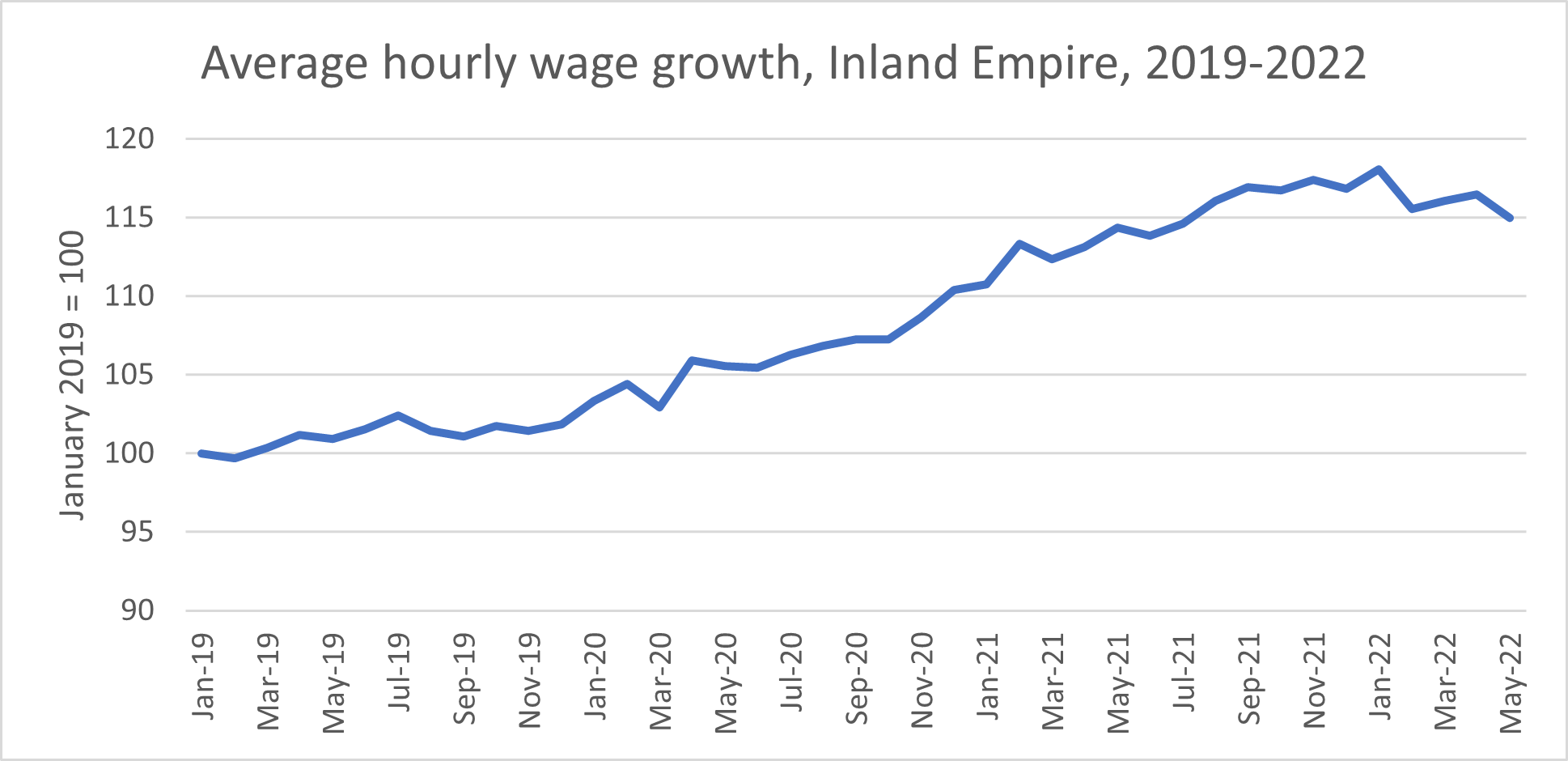

Another point of concern is hours and wage growth. For the last two months, average weekly hours have been down year-over-year (in May they went from 36.2 to 35.8), although they are still at historical highs. Wage growth has also been slower. Last year we were averaging 8%-9% wage growth, but in May of this year, we registered just a 0.5% year-over-year increase and an actual decline in level (though not seasonally adjusted). See the chart above on wages, which indexes to 100 as of January 2019. You’ll note that most of the gains in wages were made last year, and growth has considerably slowed down in the last 6 months or so. Still, the index stands at around 115 - implying 15% wage growth since January 2019. Record-high inflation has erased some of that income growth, which is why I wish these numbers were higher.